Wire

Wire

A wire transfer is an electronic payment service for transferring funds “by wire” through either the CHIPS, FedWire, or SWIFT payment systems.

Overview

- Wires most commonly used for high dollar value - low volume type transactions

- Wires can only be used between banks

- Available only during non-holiday weekdays and during business hours

- Transactions are not reversible

- Cannot be used to request funds

- High sending fees (chase pays $.15 per wire, but charges $25-45 per outgoing wire), $15 to receive..additional fees for non-USD wire, failed wires, etc…

- Fees make it impractical for small transfers, individuals can send up to $100K

- Used in payment clearing & settlement

Fedwire & CHIPS used for large value domestic & international USD payments

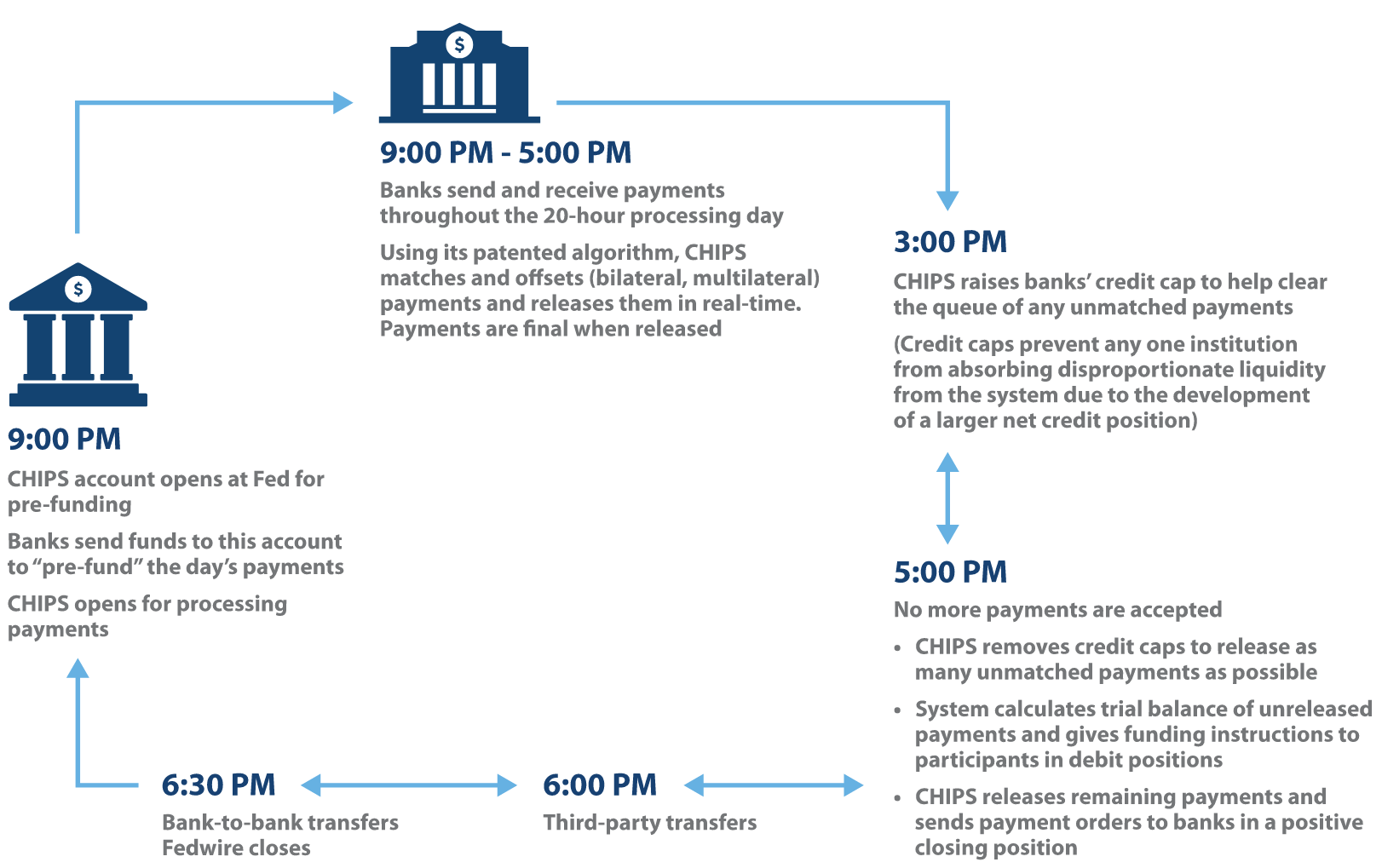

CHIPS - Clearing House Interbank Payment System

- Operated by The Clearing House (TCH) - a banking association and payments company that is owned by the largest commercial banks.

- Private sector counterpart to Fedwire

- Note: UK equivalent to Fedwire is called CHAPS and is operated by the Bank of England

- Organized in the 70’s

- Only available to ~50 member banks - by the banks that use it

- Primary clearing house in the US for large banking transactions

- It is a Deferred Net Settlement (DNS) system

- Subject to supervision and examination by the Federal Reserve and other federal bank supervisory agencies

- CHIPS is designated as systemically important by FSOC- under Title VIII of the DFA (Dodd-Frank Act)

- Generally used for large-value interbank funds transfers

- Settles roughly $1.8T every day in domestic & international payments

- Cheapest wire service & therefore the default choice for banks

- Slower but less expensive than Fedwire => is not a real-time system

- Funds are generally settled intraday => so available next day

- Funds are netted against debits & credits across all transactions at the end of the day

- Operating hours are 9AM - 6PM Eastern

Clearing - transfer & confirmation of information between the sending financial institution and the receiving financial institution.

Settlement - the actual transfer of funds between sender & receiver

Fedwire Funds - owned and operated by the Federal Reserve

- Used by US banks, credit unions, government agencies & the federal reserve

- Service users must be account holders at a Federal Reserve Bank - subject to terms and conditions specified in Operating Circular 6 and the PSR policy

- It is a real-time gross settlement (RTGS) system - more expensive than CHIPS, but provides immediate settlement on individual transactions

- Puts more pressure on banks to insure they have sufficient liquidity available to settle

- A credit transfer system - a debit entry is made to an originator’s account and credited to the receiver’s account

- Most widely used wire transfer system in the US => May 2021 => 16 million transfers totalling $75.6 trillion

- System is closed during the weekends & federal holidays => operating hours

- ISO 20022 - Federal Reserve info

- Migrating to ISO 20022 messaging format no earlier than November 2023

SWIFT - International Payments - Society for Worldwide Interbank Financial Telecommunications

- Formed in 1973 & Based in Belgium => Created by a consortium of 239 banks to faciliate cross-border payments

- Today - SWIFT connects more than 11K FI’s across 200+ countries

- Analogous to a simple email system enabling secure messages across it’s members

- Averages 40million messages/day that include orders, payment confirmations, FX exchanges and trades

- Uses standardized MT (message type) messages

- Looking to fully migrate to ISO 20022 by 2025

- Plans to test Tokenization in 2022, with participation from Clearstream, Northern Trust, SETL

- Wires typically take 2-3 days

- cutting off a nation’s banks from swift access restricts flows into and out of that nation => this can result in real economic pain