ACH

ACH - (Automated Clearing House)

- ACH is an electronic funds transfer system that facilitates the movement of money between bank accounts in the US

- Evolutionary step up from paper checks (conceived in the late 60’s)

- System designed and well suited for repetitive payments like: payroll, mortgage installments, utility payments, etc.

- also called eChecks, direct deposit, direct debit…

- Nacha - National Automated Clearing House Association - is the rule making body

- Mostly low value, but high volume

- Usually free or very inexpensive for both the sender & receiver

- ACH messages are delivered up to 5x a day (06:00, 12:00, 16:00, 17:30, 22:00) <= Eastern

- Same day ACH introduced 2016 - has current per-payment limit of $100k, set to increase to $1M in March 2022

- same day settlement but is not an RTP system…. same day is same day, not real-time

- Considered more secure than a wire.

- Good for US payments only

- Often used by Paypal, CashApp, Coinbase, etc… behind the scenes to transfer funds from user’s bank account to their respective platforms

Quick stats

- Payment volume and value statistics available here, here, and here

- $62 Trillion was processed via the network in 2020

- Volume increasing across payment scenarios, with B2B payments joining the trend (with transactions increasing 15%)

- Pandemic spurring much of adoption of electronic payment solutions => check payments declined more than 23% yoy in Q4, says the Fed.

- Same-day ACH volume spiked 35.7% in 4th Quarter 2020 -> value of transactions spiked 101% <= driven in part by increased B2B usage

Two ACH Transfer Types:

- ACH Credit

- An ACH entry that deposits funds into a Receiver’s account

- Example: payroll direct deposits

- ACH Debit

- An ACH entry that withdraws funds from a Receiver’s account

- Example: any pre-authorized bill pay scenario: mortgage payments, utility or credit card payments, etc.

Definitions:

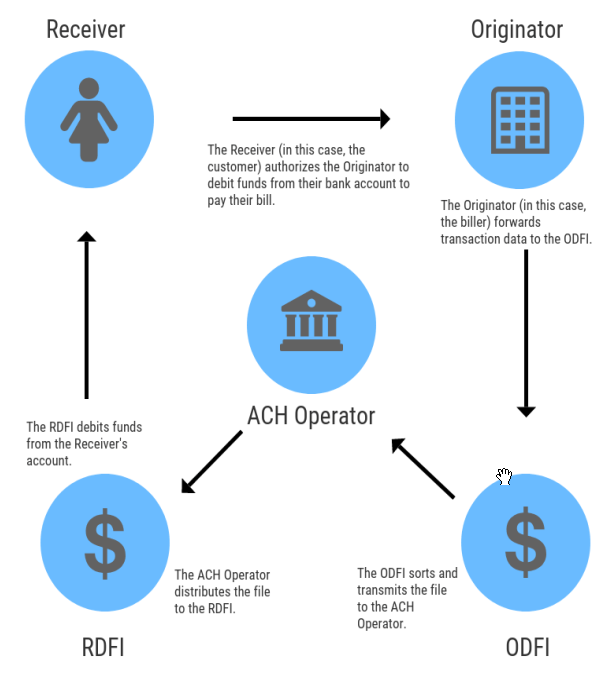

- Originator: Usually a company that initiates an ACH debit or credit, through an ODFI or Third-Party Sender, to a

Receiver (a consumer or another company)

- Can also be an individual or other entity

- Needs the Receiver’s pre-authorization

- Originator always represents the transaction “initiator” regardless of debit or credit transaction

- ODFI: Originating Depository Financial Institution - usually the originator’s bank

- The entity responsible for converting ACH transactions into a NACHA accepted formatted file and transmitting it to the ACH operator.

- RDFI: Receives the transaction and performs validation of funds availability and account standing.

- Receiver: Company or individual receiving an ACH debit or credit entry from an Originator

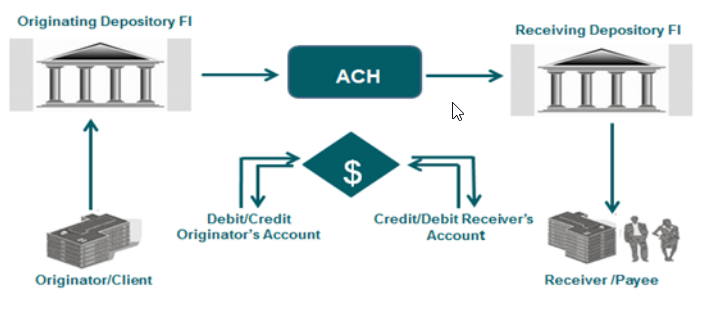

General Flow:

- An Originator– whether that’s an individual, a corporation or another entity– initiates either a Direct Deposit or Direct Payment transaction using the ACH Network.

- The Originating Depository Financial institution (ODFI) enters the ACH entry at the request of the Originator.

- The ODFI aggregates payments from customers and transmits them in batches at regular, predetermined intervals to an ACH Operator.

- ACH Operators (two central clearing facilities: The Federal Reserve or The Clearing House) receive batches of ACH entries from the ODFI.

- The ACH transactions are sorted and made available by the ACH Operator to the Receiving Depository Financial Institution (RDFI).

- The Receiver’s account is debited or credited by the RDFI, according to the type of ACH entry. Individuals, businesses and other entities can all be Receivers.

- Each ACH credit transaction settles in one to two business days, and each debit transaction settles in just one business day, as per the Rules.

Example: Workflow for a bill payment

The ACH payment network is really two intertwined systems run by two separate operators:

- EPN - (Electronic Payments Network)

- Operated by The Clearing House (TCH) - a banking association and payments company that is owned by the largest commercial banks.

- Generally services transactions between banks

- FedACH

- Operated by the Federal Reserve Banks

- Generally services transactions involving government related financial institutions

- Same Day ACH

- NACHA proposed fees of $.08, fed actions pushed this down to $.04 => good for end users