Payment Cards

Payment card is a collective term generically referring to credit cards, debit cards, or most cases of “stored-value” cards.

Credit Cards

Overview

- Credit cards combine a payment instrument with a credit arrangement => they are effectively uncollateralized short term loans

- Act as a transactional medium => substitute for cash, checks, and other payment methods

- Credit - substitute for layaway plans (BNPL) & ST bank loans - though expensive if balance is carried

- General purpose cards are generally issued by a bank under license from a payment card network (Visa, Mastercard, etc.)

- Have revolving credit limits => credit allowance renews as debt paid off

- 4 major payment networks (brands) => Visa, Mastercard, American Express, Discover

- Work in most markets globally

- CC charges are reversible

- Most commonly used for everyday mid-sized to small payments and online purchases

- Can take anywhere from 1 - 3 days to process completely (authorize => settlement, not real-time payment method)

General biz strategy - provide the infrastructure, leverage marketing & incentive programs to increase transactions (volumes & values) => build the highway & collect tolls for use. Widespread issuance of cards + global marketing have made the card networks some of the most recognizable brands in the US

Visa - See Visa Crypto Strategies

Quick Stats

- Can authorize ~1.7k transaction per second

- Can process ~150 million transaction per day

- ~188 billion purchase transactions made worldwide in 2020 (40% of ALL credit card purchases)

Comprehensive Stats @ Cardrates

- In 2019, there were 39.6 billion purchase transactions in the US across all credit card schemes (Visa, Amex, etc.)

- Works out to be roughly 108.6 million

- 1.06 billion credit cards in use in the US => US Population ~330 million

- Credit card use has increased from 18% to 23% between 2016-2018

- Contactless transactions have increased in recent years

- Apple Pay accounts for 5% of all global cc purchase volume

- Estimated to reach 10% of global cc transactions by 2025

- Visa cards accounted for 44.84% of transactions worldwide

- Matstercard cards accounted for 24.46% of transactions worldwide

Definitions

- Issuer - a financial institution that issues branded cards (by a payment network)to a cardholder (consumers or businesses), they are responsible for sending payments

- Acquirer - a Financial institution that enrolls merchants to accept payments, processes payments on their behalf, ensures they are paid for each transaction, they receive payments

- Merchant - any business that accepts (visa, mastercard, …) as a payment through Point-of-Sale device or online transaction

- Cardholder - any consumer or business that uses a card to make purchases

- Payment Processor - manages the transaction process => acts as mediator between the merchant and financial institutions involved

- Transactor - a cardholder that pays off their balance each month => ~31% of account holders

- Revolver - a cardholder that maintains a balance each month => ~40% of account holders

- Once consumers begin to revolve an account, they do so continuously on average for about 10 months => ~15% of these will revolve continuously for two years or more. The longer a balance is revolved, the higher the chances the balance on an account will continue to revolve.

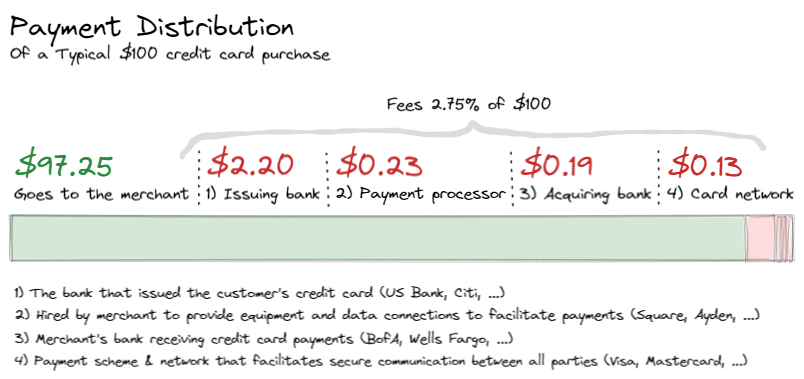

Merchant Discount Fees (MDF)

Merchants pay a small collection of fees to various payment facilitators in order to accept credit card payments.

- Interchange fee: Goes to the issuing bank - the largest single chunk of the fees

- Card scheme fee: Goes to the payment network (Visa, Mastercard, etc)

- Acquirer and processing fees: Divided between acquiring bank & payment processor

Example:

A consumer pays a merchant $100 for goods and services rendered. The $100 is roughly distributed across the merchant and payment facilitators as follows:

Card-present vs. card-not-present

Card-present (CP) transactions (aka in-person transactions) have lower interchange fees than card-not-present (CNP) transactions (ex. ecommerce). This is because the risk of fraud is lower when the customer’s card is physically present.

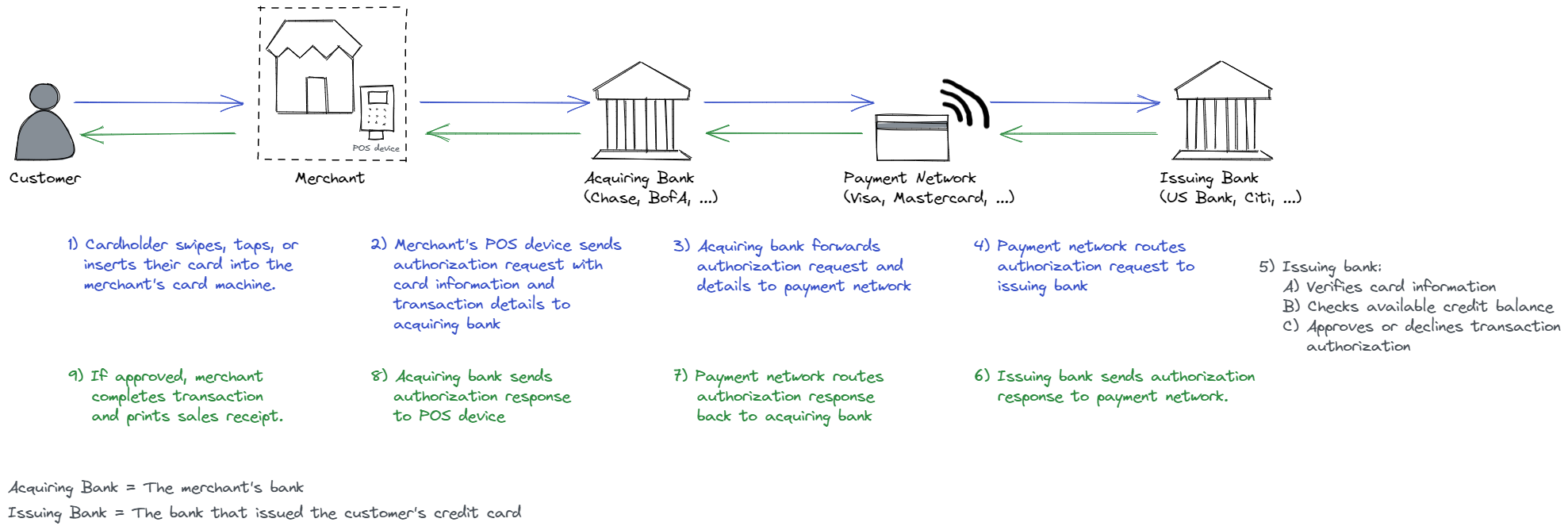

Credit Card Processing Flow

This is an illustration of the steps and parties involved behind the scenes when a credit card is used to pay for goods or services.

Step 1 - Authorization, Authentication, and Capture

In this stage, the merchant seeks a transaction authorization from the cardholder’s bank. If the request is approved the cardholder’s bank deducts the transaction amount from the cardholder’s credit limit and the merchant proceeds to complete the transaction with the customer.

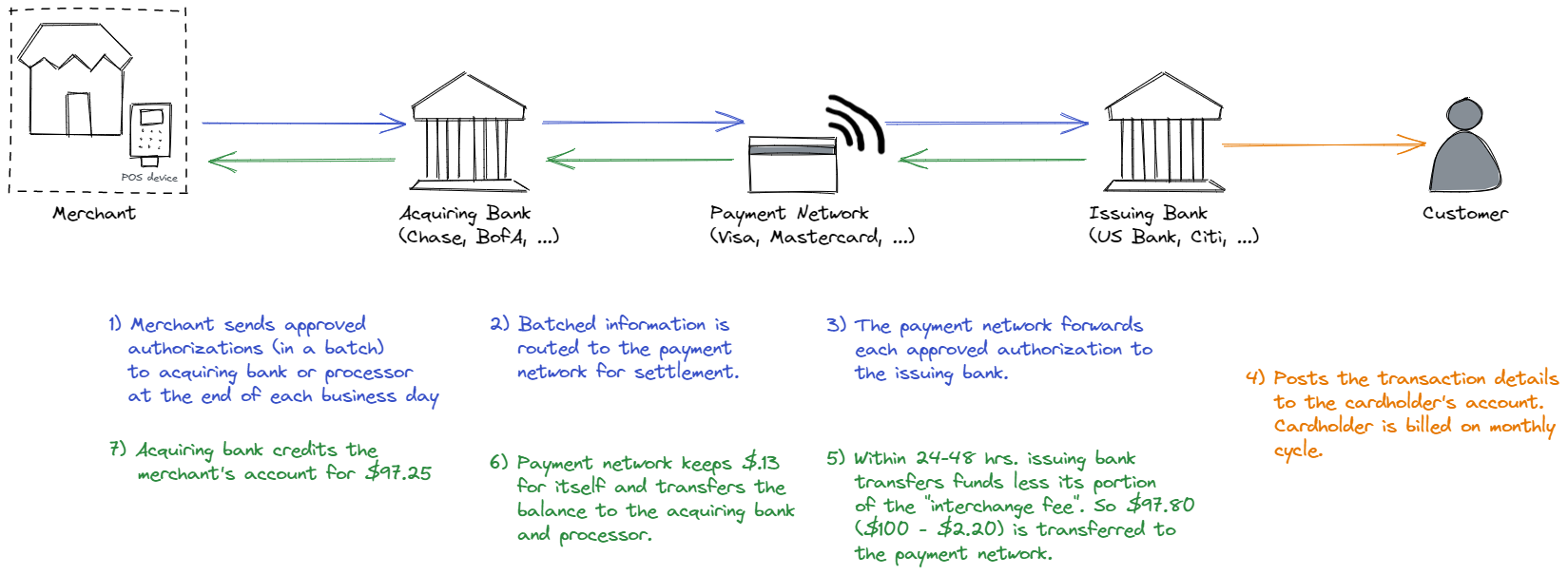

Step 2 - Settlement and Funding

At the end of each day, merchants send their authorized charge transactions in a batch to the their payment processor or acquiring bank. The transactions are submitted to the payment network and routed to each issuing bank. After a few days time, issuing banks send payment less their share of interchange fees. Payments are routed through the payment network and deposited into the merchant’s account at the acquiring bank less interchange fees. It can take 2-3 business days from the date of the transaction before the merchant sees the funds in their account with the acquiring bank.

Network Models

Open Loop vs. Closed Loop Systems

- Open Loop - credit or debit cards that can be used to pay for purchases at any merchant or business. Any card sporting the Visa or Mastercard works in an open loop environment.

- Close Loop - Merchant/Store issued credit cards, can only be used within that system.

Revenue Levers <= For Providers

- Net interest => The interest charged on any balances not paid in full each month => avg. credit card interest rates are 16%

- Represents roughly 60% or more of total earnings

- Interchange => illustrated above, the fees earned by the issuing bank for it’s role facilitating a credit card purchase

- Represents roughly 15%-30% of total earnings

- Card Reward Programs carve out a percentage of Interchange to pass along to the card holder

- Fees => Annual fees, late fees, etc. => but many have generally fallen out of favor…

- Marketing contributions - newest revenue lever - marketing campaigns, often in apps, to nudge buyer behavior towards certain brands then invoice businesses for marginal revenue generated, ex. Cash App’s “Boosts”.

Consumer Benefits

- ~30 Day Short Term Loan

- Rewards Programs (points, cash back, etc.)

- Limited liability for fraudulent charges

- Sometimes Warranty protections

- Ease of Use

CARD Act of 2009 (pdf)

- Law designed to protect credit card users from abusive lending practices by card issuers.

- Primary goals were the reduction of unexpected fees and improvements in the disclosure of costs and penalties.

- Estimated to have returned over $10 Billion a year to consumers

Security & Tech

-

PCI Compliance

-

Mobile Wallet - virtual wallet that stores a user’s card details on a mobile device. They can be used to make payments instead of using a physical card

-

NFC/Contactless Cards

Contactless Cards (wifi)

Other Resources

Reports & research

- ABA - Credit Card Market Monitor

- Statista Data

- The Effects of the COVID-19 Shutdown on the Consumer Credit Card Market: Revolvers versus Transactors - 2020

- Data Point: Credit Card Revolvers - (pdf link)

- Who Gains and Who Loses from Credit Card Payments? - 2010 - (pdf link) - Exec Sum

- Credit Card Interchange Fees: Debunking Six Myths - 2008

- The Merchant-Bank Struggle for Control of Payment - 2006

- The economics of credit cards - 2000 - (pdf link)

- Costs and competition in bank credit cards - 1987 - (pdf link)

Debit Cards

- A debit card is a payment card that immediately deducts the payment amount from a consumer’s checking account when used.

- Are generally issued by a bank under license from a payment card network (Visa, Mastercard, etc.)

- One of the fastest growing non-cash payment types in the last decade

- Processed using either single message systems or two-message systems.

- A single-message system is based on ATM/POS network technology that combines authorization and clearing into one step in which transactions are usually authorized by entering a PIN number into a merchant’s POS device.

- A two-message system is based on credit card processing systems, where authorization is completed in the first step and clearing is completed in a second step.

- Over 60% of debit card transactions were authorized using a two message system, virtually all of which were processed over the Visa and Mastercard networks.

- There are also several smaller debit card networks operating in the US beyond Visa & Mastercard

- Over 60% of debit card transactions were authorized using a two message system, virtually all of which were processed over the Visa and Mastercard networks.

Visa Direct & Mastercard Send Visa Direct can handle business-to-business (B2B), business-to-consumer (B2C) and person-to-person (P2P) payments. “Instant pay” features for Venmo, PayPal, Lyft and Postmates all use Visa Direct. Like the RTP network, Visa Direct is a credit push system, though it moves money on the debit card rails. Transferred funds are available within 30 minutes after a transaction is completed – even on nights and weekends – and sometimes much sooner.

Prepaid Cards

- Have grown substantially over the past decade.

- Many are reloadable

- Facilitate access to non-traditional financial accounts

- Are sometimes used as a substitute for a traditional bank checking account,

- Cards can be issued for and payroll and government benefit to take the place of pay checks and government benefit cheques.

- Prepaid cards include specific-purpose restricted-use EBT cards provided by governments, private label and general purpose gift cards issued by retail merchants, card networks, and certain rebate cards.

- In 2009, prepaid cards were used for 6.0 billion transactions valued at $142 billion.