Banking

These are notes on how the US banking system works.

Central Bank

The US Federal Reserve system (Federal Reserve Board and twelve Federal Reserve banks) is the central bank of United States. The system is divided in 12 districts, each with a separate reserve bank. The Federal Reserve banks issue money and provide payment services to facilitate transactions between financial institutions. Created in 1913 - fallout from banking crisis (they were failing) in 1907. Federal Reserve is the lender of last resort now, but in 1907 it was JP Morgan (the person).

The Federal Reserve System performs the following core functions:

- Conduct monetary policy => Performed by the Federal Open Market Committee (FOMC)

- Three policy levers: open market operations, setting the discount rate, and reserve requirements

- Framework based on “Dual Mandate” to foster economic conditions that achieve both stable prices and maximum sustainable employment => created in 1977, significantly updated in Aug. 2020.

- Promote stability in the financial system

- Promote the safety and soundness of financial institutions

- Promote consumer protection

- Provide and facilitate payment and settlement systems for depository institutions.

- Function as a settlement agent between commercial banks in large value payment systems by transferring deposits held at the central bank from one commercial bank’s settlement/clearing account to another.

- Regulate and supervise the banking system

- In essence, they manage money => the supply and price

- Supply => Monetary base => M1, M2, M3.

- Price => Interest rate Open Market Operations

- Modern Central Banking began ~1971 with the end the Bretton Wood System.

- TLDR Version - Central Banks:

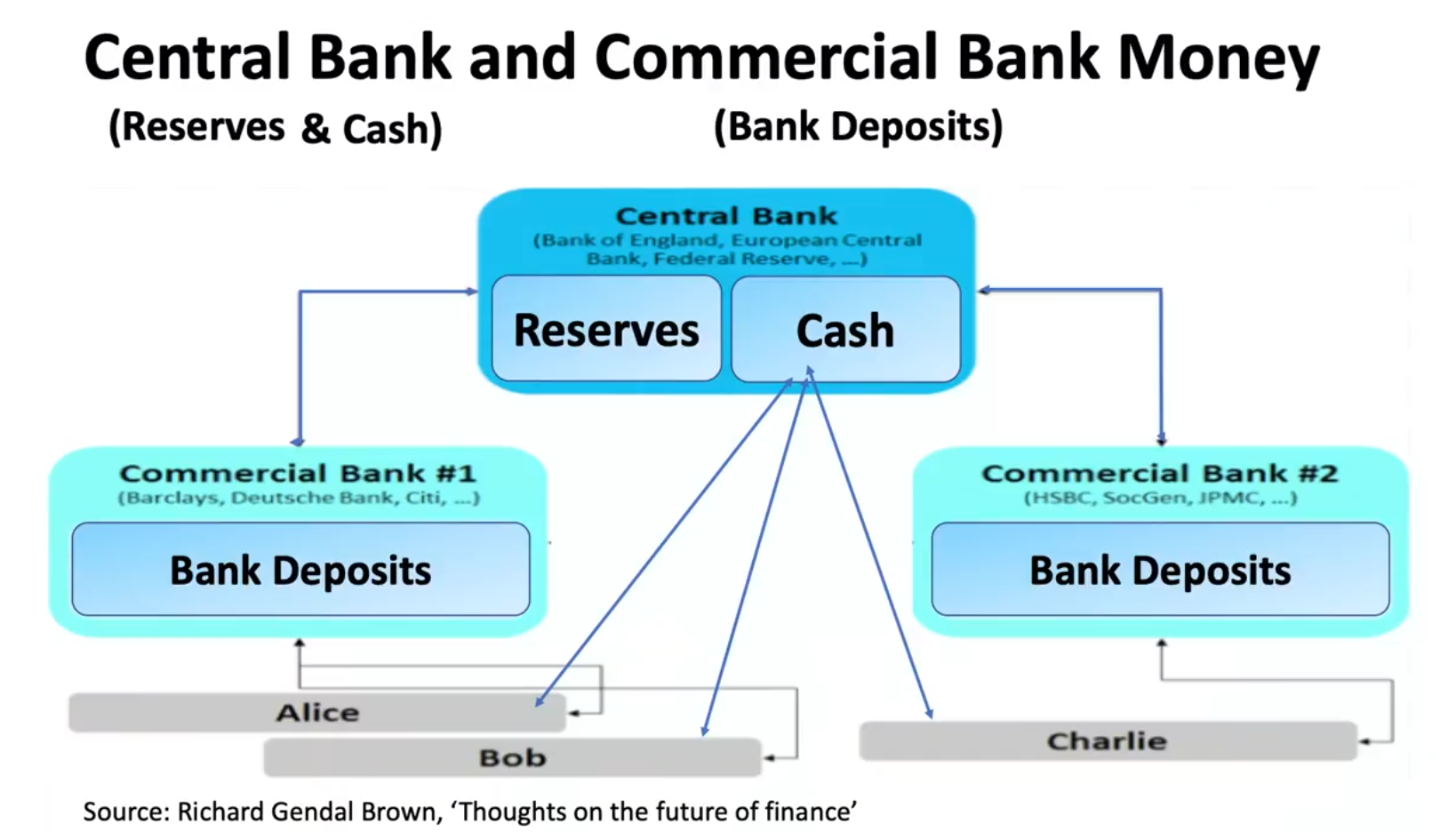

Central Bank Money

-

The Central Bank holds comercial bank (and other FI’s ) reserves (deposits) and is reponsible for producing the cash in circulation

- See Bank Reserves

-

Commercial banks hold customer deposits (liabilities) => commercial banks further expand the money supply by making loans => see Fractional Reserve Banking

-

Currency => Federal Notes & coinage

- Paper Bills: Produced by The US Treasury’s Bureau of Engraving and Printing

- Coins: Produced by the US Mint

- Note: Paper bills & coins are a tokenized means of money => a representation of value being held at the Federal Reserve

- They represent a liability of the Federal Reserve

- See notes on Central Bank Digital Currencies (CBDC’s)

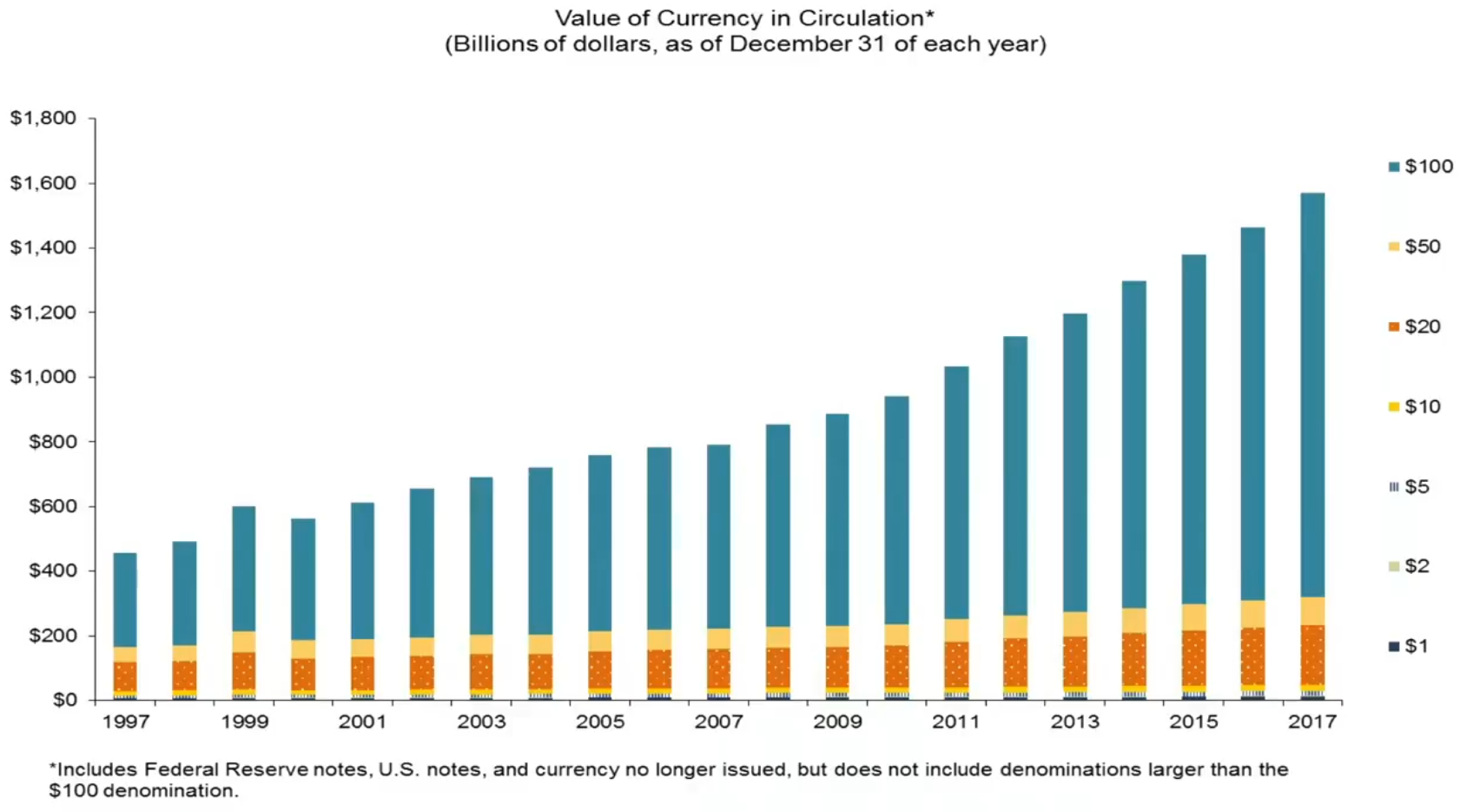

- US economy valued at roughly $20 Trillion => currency makes up about 8% @ $1.6T => current currency data

- Over half of the $100 bills is thought to be held internationally (overseas)

- Smaller bills have a higher velocity => they exchange hands faster & wear out quicker than higher bills ($1’s last ~18 months, $20’s 3-5 years)

- As goods and services become more expensive over time, circulation of smaller denominations should drop as they become less useful …ex. half dollars are rarely used today while they used to be very common before the 70’s.

-

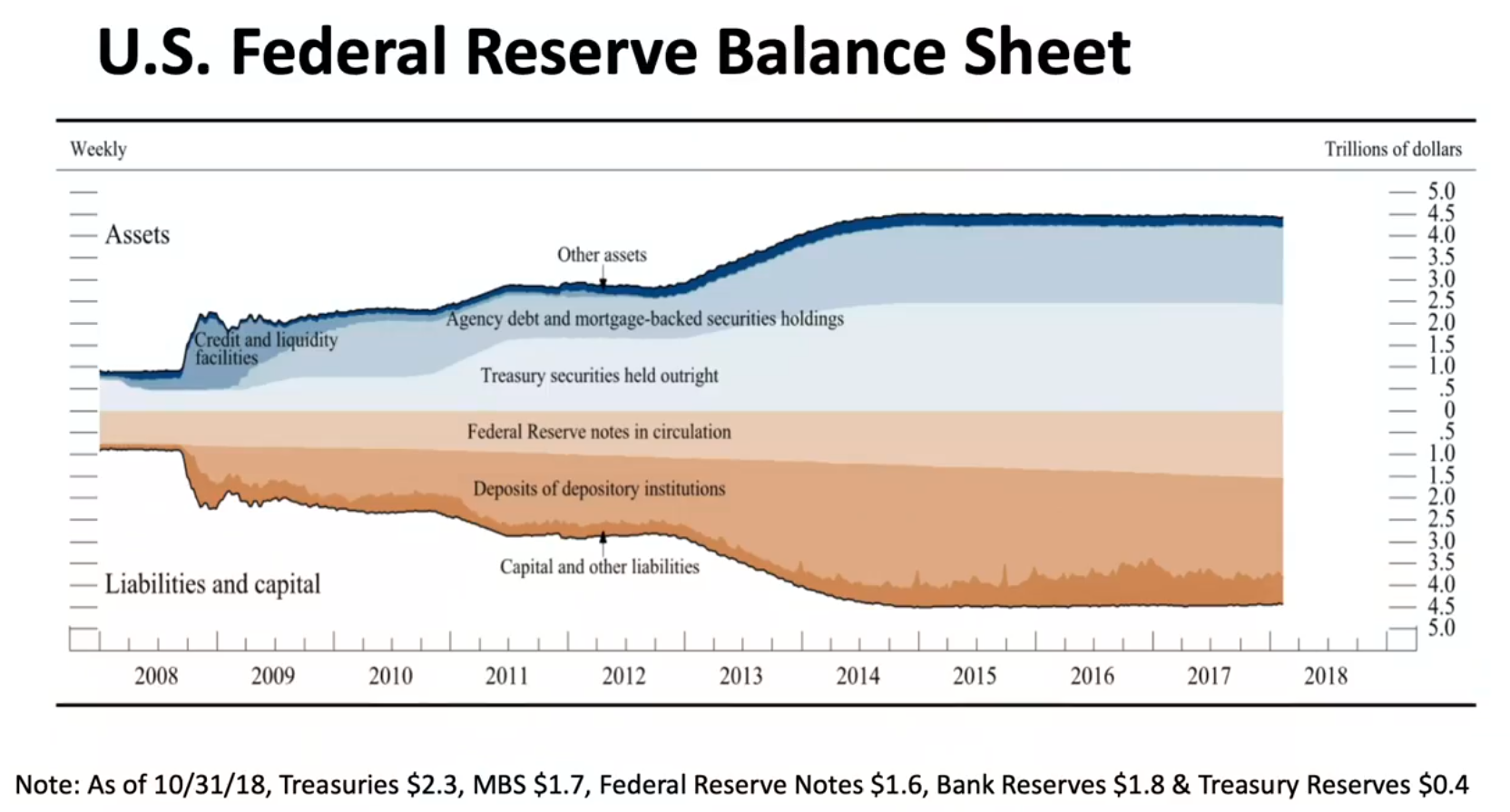

Federal Reserve Balance Sheet - a list of all its assets & liabilities

- Link to representation showing the impact of Covid (need to scroll)

- Link to representation showing the impact of Covid (need to scroll)

Important Legislation:

- Federal Reserve Act of 1913

- Established the Fed as America’s central bank

- …More history about the Fed (…a timeline)

- Banking Act of 1933 (Glass-Steagall)

- Separated commercial banking from investment banking, created the FDIC, …among other things

- Gramm-Leach-Bliley Act of 1999

- An attempt to update and modernize the financial industry, most notable inclusion was the repeal of portions of the Glass-Steagall Act - allowing investment & commercial bank the freedom again to merge service offerings

- The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (DFA)

- Provides additional authorities for these or other relevant regulatory agencies over payment, clearing and settlement systems designated by the new Financial Stability Oversight Council (FSOC) as systemically important.

- One of the most significant pieces of legislation affecting the US financial regulatory framework in many years.

- Full list of relevant acts & regulations

Commercial Banks (Retail)

Commercial Banks are financial institutions that accept deposits, offer checking and savings account services and makes loans. But they are more than that..

They are an important part of the economy providing vital services for consumers and businesses alike.

- Banks accept deposits from consumers and businesses => these deposits become the funds banks loan to consumers and businesses => these loans grow the economy because they are being spent => which eventually become deposits again => this cycle has the net effect of expanding the money supply in the economy.

Thus, banks help create money through a process known as Fractional Reserve Banking (“Part 2” => relevant section)*. The money created by banking activity is known as “deposit money” or “inside money”. It is the dominant form of money in modern economies today => most commercial transactions are ultimately transfers from one deposit account to another deposit account. If deposit money is inside money then physical currency (that created by the Federal Reserve) or “central bank money” is known as “outside money” (NOTE: bank reserves are also outside money and technically the more important monetary instrument helping the Fed achieve its policy goals). Worth highlighting here, how it is outside money that serves as the conduit to jumpstart the inside money creation cycle.

- As of November 2021, deposit money (in various forms) accounted for roughly 90% of the M2 Money Supply measure => central bank money accounted for ~10%.

- List of the Biggest Banks by Total Deposits

- Deposits represent a liability to commercial banks, whereas a loan is considered an asset. Here’s what a simplified bank balance sheet could look like:

Banks earn revenue primarily through interest charged on loans and earned on securities investments, but also though a variety of other services and credit card programs (both as an issuer and/or acquirer).

* In theory, I could become a bank. To start, I could collect deposits from customers, let’s say an initial $100k. I’d save 10% as a reserve and then lend the other $90K to other customers => this proess can be repeated many times. This effecctively increases the money supply => more people have access to dollars and the ability to spend them. Unlike physical currency, these dollars really are just digits stored on in a database. => Also see Bank of England paper: Money creation in the modern economy.

Investment Banks

Product services at investment banks differ quite a bit from traditional banks. Clientele also tends to skew towards governments, large corporations, other financial institutions and large investors.

Investment banks are typically structured into different product groups covering:

- Mergers & Acquisitions (M&A) - Advise or faciliate the mergers of companies with one another

- Leveraged Finance - Provide services to companies to finance corporate activities by issuing high-yield debt.

- Equity Capital Markets (ECM) - Provide services to companies or corporations on the issuance and management of IPOs, bonds, and stocks.

- Restructuring - Offer services to help companies or corps. with restructuring to improve profitability and efficiency.

Link to the Top Investment Banks.

While commercial banks help the economy by expanding the money supply and allocation of credit, investment banks help the economy in other ways, mainly through intermediation (=>fed speech) in the capital markets. Investment banks underwrite debt and equity securities and match buyers and sellers to provide liquidity to the financial markets. Buyers have access to investment opportunities while large companies have access to a large variety of financing opportunities. This exchange facilitates a process known as capital formation => in essence it helps companies better finance their activities to expand and produce goods and services for the economy.

Big Picture

An overly simplified view of how all of this comes together:

- The Fed (central bank) creates physical money to inject into the initial money supply and jumpstart the cycle

- Commercial banks, by accepting deposits and issuing loans, expands the money supply exponentially

- This means MORE people and companies have access to money for purchases and savings.

- Investment banks help large corporations source funds (from step 2) to invest in research and production capabilities to expand product and services available for sale in the economy.

- The Fed and related governmental agencies (OCC, SEC, CFTC, and others) have oversight responsibilities over both commercial and investment banks. The Fed also possesses regulatory levers to nudge these banking institutions (and their activities) towards different policy objectives => changing over time and influenced by market activity and other priorities.

- Repeat steps 1-4